dLocal (DLO): DCF Valuation

+1.29%current return

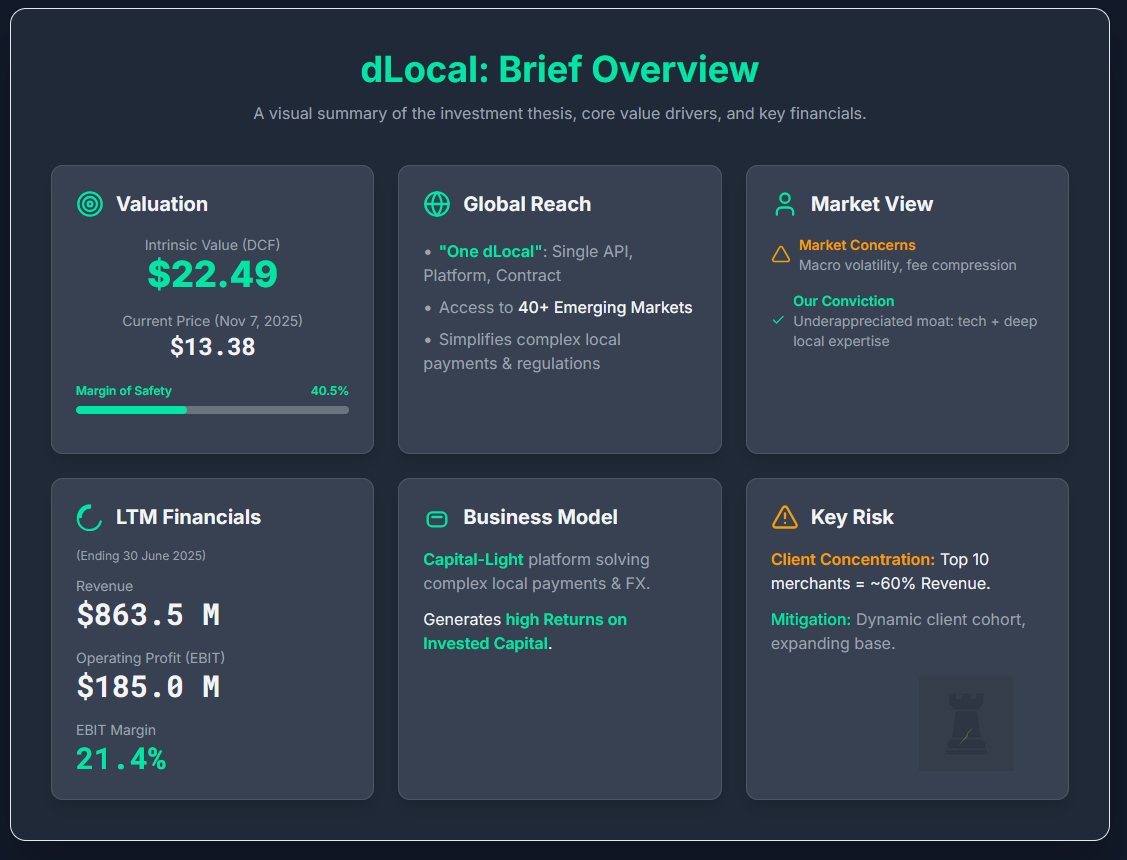

"Brief Overview dLocal Limited (DLO) operates as a critical, technology-first payments platform, providing the financial infrastructure that connects global enterprise merchants with billions of consumers in fragmented and complex emerging markets. This focus, however, seems to underappreciate the durability of dLocal’s moat, which is built not just on technology but on deep, localised operational expertise that is difficult and costly for competitors to replicate at scale. Business & Financial Context dLocal’s core business is simplifying cross-border payments for global merchants through its proprietary “One dLocal” concept. As of the last twelve months (LTM) ending 30 June 2025, dLocal generated revenue of $863."

Date of Analysis: November 5-7, 2025 Verdict: Undervalued Current Price Target (Base Case): $22.49 Price at the Time of Analysing: $13.38 1. Brief Overview dLocal Limited (DLO) operates as a critical, technology-first payments platform, providing the financial infrastructure that connects global enterprise merchants with billions of consumers in fragmented and complex emerging markets. The fundamental driver of its economic value is a capital-light business model that enables the company to gene

Entry:$13.59

Target:$22.49

Horizon:Short-term

Trade CallBullish

Medium Conviction

idea •HatedMoats • Nov 7, 2025

Opening new positions - DLocal Limited

"DLO: Competition intensifying in LATAM (especially Brazil/Mexico) as major payment processors enter market. Poor corporate governance with questionable dividend policy. Customer concentration risk (two clients >10% of revenue). Current valuation offers downside protection. PayPal partnership positive. Strong CEO (Pedro Arnt)."

— The Reservist

Entry:$10.02

Target:N/A

Horizon:Expires Jun 19, 2026

Trade Callbullish

Medium Conviction

Stock Idea •The Reservist • Jun 19, 2025

DLocal, a new invest and investigate!

"DLO: Emerging market payment processor, 92% 6yr TPV CAGR, 25% forecast EBITDA growth. 13x NTM EBITDA. Strong mgmt, sticky biz w/ top clients. Risks: declining take rate (1.4% to 1.1%), margin pressure from headcount growth. Huge TAM, but competition & fintech landscape unclear. Invest & investigate further."

— The Reservist

Entry:$8.22

Target:N/A

Horizon:Expires Mar 10, 2026

Trade Callbullish

Medium Conviction

Stock Idea •The Reservist • Mar 10, 2025